The property market is booming. Large amounts of money are gambled on land that only yesterday was paddock or scrub. Banks compete to outdo each other in lending to miners, developers and speculators, financed and reliant on a continual flow of foreign investment. Newspapers celebrate a golden future and politicians promise endless growth. The whole country seems to run on the assumption that tomorrow will always be richer than today. You might think this is modern Australia — but it is not. It’s 1893, and we are on the edge of our first great banking crash.

To understand what happened, we need to walk the streets of what was proudly called “Marvellous Melbourne”. Victoria was barely three decades old as a separate colony, carved out from New South Wales in 1851, and the city of Melbourne itself had been seized from the Kulin nation in an illegal treaty less than half a century earlier. It was a young settler society built quickly and brutally, first on gold, then on wool, and finally on credit.

Over in the United Kingdom, investors were intoxicated by the promise of Australia. Around 10% of British foreign investment flowed to this distant colony. 70% of Australia’s imports and up to 80% of its exports were tied to Britain. The empire’s money men saw Australia as a frontier of easy returns, a place where land could be bought cheaply, subdivided, and sold dear.

British banks lent heavily to Australian banks. Australian banks, flush with borrowed cash, lent even more heavily to property developers and mining ventures. At its peak, net foreign liabilities exceeded 150% of GDP. For every pound circulating in the local economy, Australian institutions owed one and a half pounds to lenders in London. It was a house built on credit.

Local banks had what seemed like a delightful problem. They had too much money to lend. The only catch was that it was not really theirs. It was borrowed from Britain, and it came with expectations. The plan was simple: take British money, pump it into land and mines, watch prices rise, repay the loans, then pocket the difference. As long as the boom continued, everyone would win. And for a while, it felt like everyone was winning.

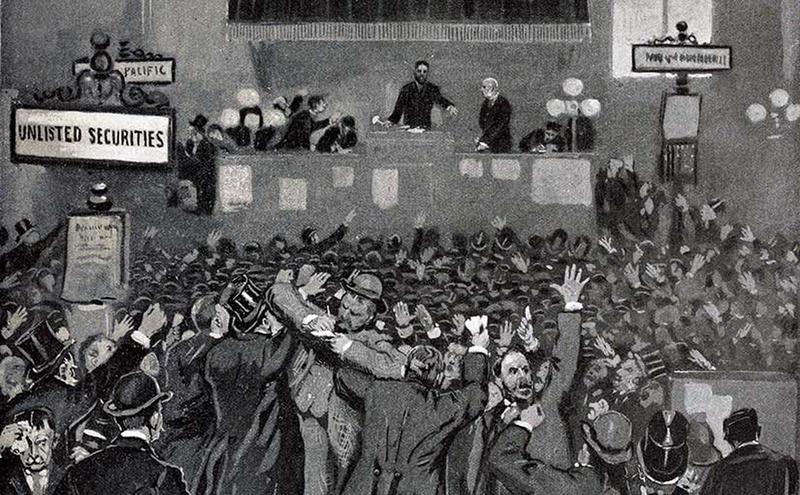

CREDIT: ART GALLERY OF NSW

By the 1890s, Melbourne had reached a size larger

than most European capitals at the time.

Grand multi-tiered buildings rose all along Collins Street. Speculative subdivisions crept further and further out from the city. Railways were laid across the country. A newspaper in 1880 noted that a married couple in Australia might earn between £90 and £100 a year, compared to around £65 for an English family. It seemed certain that the colony had escaped the poverty and squalor of the Old World… but there was a catch.

Those higher wages were devoured by higher living costs. Rents soared. The price of land became detached from any sensible measure of value. In 1888, houses in Prahran were selling for more than £1,000, a figure that would not be matched again for sixty years. Families stretched themselves thin to secure a foothold in the market. Builders borrowed to buy more land to build more houses for buyers who were themselves borrowing.

By the end of the 1880s, more than 70% of Australia’s GDP was tied to bank credit. Nearly every part of economic life rested on borrowed money and the assumption that land values would keep climbing. Union leader William Spence would later describe it as a “period of capitalism run mad without let or hindrance.” Then the music slowed.

International economic conditions shifted. Confidence wavered in London. Investors began to question whether the returns were as safe as they had been promised. The flow of easy credit tightened, projects stalled, and developers struggled to sell at inflated prices. As usual, the first to feel the effects were working people.

When investment slows, it is not the shareholder who loses their weekly pay. It is the labourer, the clerk, the carpenter. As loans were called in and businesses folded, wages went unpaid. Properties were seized. Then, in 1893, the banks themselves began to fall. On 5 April 1893 the Commercial Bank of Australia, then Victoria’s largest bank, shut its doors. Within weeks, 13 of Australia’s 22 trading banks had suspended operations. Crowds gathered outside bank doors, desperate to withdraw savings before it was too late.

In January 1893 the Victorian Premier admitted that “15,857 persons were registered as unemployed.” In Melbourne alone, nearly a third of workers were suddenly without a job. Across the colony the economy contracted sharply, with output falling by roughly 17% over two years. What had been called progress only months earlier, now meant hunger.

The newspapers painted scenes of quiet devastation. The Age visited the slums of Collingwood and South Melbourne and described “the kitchen with its empty shelves, the fireless grate, the solitary crust on a plate… placed high up on the dresser to be out of the reach of the children.” The woman of the house was “beside herself” and broke into tears, wondering “how long you yourself could endure such a condition of affairs.”

Children in rags queued at soup kitchens. Men roamed the streets in search of work that did not exist. Relief societies handed out bread and tea, but charity was no substitute for wages. The boom had been built on borrowed money from abroad, but the bust was paid for at home.

CREDIT: STATE LIBRARY OF NSW

Relief socities distributed aid to poor families, but it

was far from enough to meet everyone’s needs.

Behind the scenes, governments did one thing for capital and another for workers. When the Queensland National Bank collapsed, it held almost £2.5 million in government funds. Around 7,700 depositors had claims totalling £4.18 million. Rather than let the institution fail, the colonial government rushed a Guarantee Bill through parliament in a single night to protect it. Shareholders and depositors were shielded. The system was stabilised.

No such urgency was shown for the unemployed. As future Prime Minister James Scullin later reflected, “Australian workers came to realise that the forces of Government, backed by the police, the courts, and the military, were behind the employers in every struggle.” The depression, he wrote, “brought poverty and misery to thousands of homes.”

This pattern is painfully familiar. In 2008, when global credit markets froze during the Global Financial Crisis, the Australian Government guaranteed bank deposits and wholesale funding within days; stability for finance was treated as essential, but other economic stimulus given out to working people took weeks or months and was heavily criticised by economists, politicians, and the media as reckless.

CREDIT: DAVID GRAY / REUTERS

Working-class people were not the priority in the

government’s response to the Global Financial Crisis.

Even though it was the support and stimulus for working people that

ultimately saved Australia from the worst of the recession, this was never acknowledged, and it is still characterised by many as “pseudo-economics”.

In the 1890s, investors in London did not lose sleep over families in Collingwood or Fitzroy. They sought to protect their own money. Today, global investors do not worry about renters in western Sydney or mortgage holders in outer Brisbane. They only care about the

interest rates, commodity prices, and yields.

Australia sits at the edge of the world map, far from the great financial centres, yet is deeply dependent on them. Foreign capital flows in when returns are high, and out when risks rise. When it flows in, we build apartment towers and expand mines. When it flows out, we talk about tightening belts and restoring confidence. It has always been the same model. Dig it up, ship it out, and sell houses to each other.

That model did not end in 1893. It was echoed in the Great Depression. It resurfaced during the Global Financial Crisis. It continues in the 21st century housing market, where young people take on enormous debts in the hope that prices will keep rising.

We are told this is simply how a modern economy works. We are told that foreign investment is a blessing and that speculation is the price of prosperity. But history suggests something else. It suggests that this pattern is not natural. It is the product of political choices about who the economy is for.

In the 1890s, workers did not accept the crash quietly. Unions organised unemployed relief committees and strike funds. Meetings demanded public works and criticised the bankers. Union-run newspaper The Worker ran exposés of bank balance sheets and called for royal commissions. Out of the maritime strikes and shearers’ struggles of that decade grew a political movement determined to give working people a voice in parliament.

CREDIT: GETTY IMAGES

The trade union movement fought back hard against an

economic paradigm which unfairly punished workers.

Labor parties formed across the colonies and united upon Federation in 1901. The eight hour day, wage arbitration, old age pensions, workers’ compensation and later the welfare state were not gifts from

enlightened, benevolent capitalists. They were victories won by organised labour.

William Spence and others spoke not only of better wages but of deeper change. They talked about co-operative enterprises, public control of credit, and democratic ownership of industry and the economy. They understood that as long as finance was left to chase speculative gains, the cycle of boom and bust would continue. They imagined an economy organised around human need rather than speculative profit.

That vision has never been fully realised. Instead, Australia has oscillated between exuberance and anxiety, between celebrating the latest boom and bracing for the next bust. Our dependence on foreign capital has remained. Our industrial base has narrowed. Our economy has not become more complex or as diversified as it should be. Our prosperity has relied heavily on minerals beneath the ground and ever rising house prices above it.

CREDIT: THE AUSTRALIA INSTITUTE

The vast majority of Australia’s resources (for example,

natural gas) are exported rather than used domestically.

The story of 1893 is not just a historical curiosity. It is a mirror. When we look into it, we see the outlines of our present economy. We see the same faith in endless growth. We see the same concentration of risk in property and resources. We see the same vulnerability to shifts in distant markets. And we see, once again, that when the cycle turns, it is working people who bear the brunt.

But we also see something else: that even in the depths of crisis, there were people who refused to accept that this was the only possible future. They organised unions. They built political movements. They fought for an economy that would not treat them as collateral damage in someone else’s investment strategy. As Scullin observed, Labor itself was born to prevent that kind of misery repeating. That is the future we forgot.

The boom and bust of 1893 teaches us that Australia does not have to remain an economic colony, forever dependent on the moods of foreign investors and the price of minerals. We can choose to diversify. We can choose to build public institutions that serve communities rather than speculators. We can choose to strengthen unions and democratic control of the economy so that when the next international downturn comes, workers are not left alone to pick up the pieces.

The cycle of boom, bust, repeat, is not a law of nature. It is a political choice — and there is an alternative.

-30-

This article was originally published in Keep Left #1.

Leave a Reply